China’s fiscal policies need to play a bigger role in helping the economy since cutting interest rates would likely encourage people to save rather than spend, according to a former central bank official.

Sheng Songcheng — a former director of the People’s Bank of China’s statistics and analysis department — argued that China’s macroeconomic conditions are not suitable for sustained rate cuts. Authorities should instead consider issuing more central government bonds and making more cuts to bank reserve requirements, he said.

Sheng, who is now a professor at the China Europe International Business School in Shanghai, explained his views in an interview with Bloomberg News. It has been lightly edited for clarity:

Based on your research, what is your view about the impact of interest rate cuts on consumption in China’s current economic environment?

When interest rates fall, they have two effects: a “substitution effect,” when immediate consumption becomes more attractive, and an “income effect,” when people expect lower future income on savings. The “income effect” is playing the leading role for the time being.

Chinese households are suffering from a weakening of income expectations and have become more risk averse. Interest cuts may erode household wealth income and accelerate precautionary savings, thus resulting in a reduction in consumption at present.

Why do you think business investment is not currently very sensitive to interest rate cuts?

Enterprises focus more upon profits and risks when making investment decisions, and thus small changes in interest rates show little significance. The Chinese economy is still in the process of a recovery, and the profits of Chinese enterprises are relatively low, as shown by data on industrial enterprises. Under those circumstances, enterprises are cautious about investing and borrowing.

It’s harder for small and medium-sized enterprises (SMEs) to get financing in China, as is the case in many countries. As a result, SMEs’ investment decisions mainly depend on the accessibility of loans, rather than interest rates.

Investments by Chinese state-owned enterprises have little interest elasticity, either. This is because their financing budgets are usually less restrictive. Therefore, interest rate adjustments will not have a significant impact on the investment decisions of Chinese enterprises for the time being.

What role should fiscal policy play in supporting China’s recovery?

The latest CPI and PPI documented a negative month-on-month growth this June, implying insufficient demand for consumption and investment.

Radical policy stimulus is not recommended. A more practical approach is to expand transfer payments from the central government to local governments, or take on debt by means of treasury bonds. The leverage of the Chinese central government is low compared with other countries, while the debt quota of local governments should be under strict control.

The way to allocate these resources also matters. What China needs for the economy to pick up and grow sustainably is to support consumption and the high-tech sector.

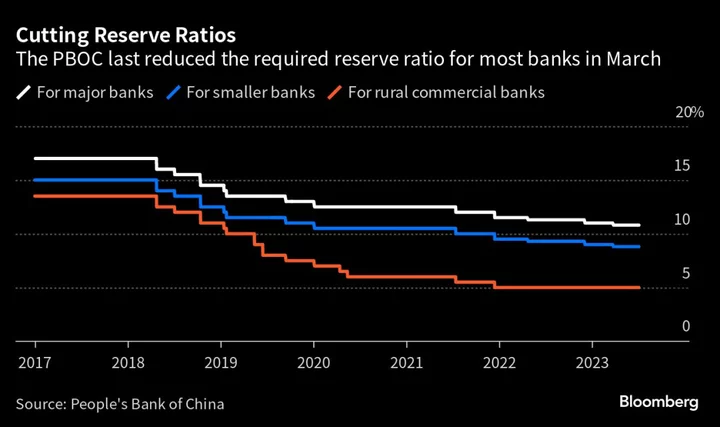

In addition, I’m inclined to think the coordination and cooperation of fiscal and monetary policy is vital. For instance, lowering the required reserve ratio of commercial banks also works for better coordination between fiscal and monetary policies, by effectively supporting the issuance of government bonds.

Does the recent yuan weakness give another reason to hold off on rate cuts?

The overall stance of China’s monetary policy is to prioritize internal equilibrium and balance it with external factors.

Whether to adjust interest rates requires a comprehensive consideration of various factors. The exchange rate is one, but it may not be the most important.

Now that the interest hikes of the Federal Reserve have almost come to an end, and the economic conditions of China will hopefully pick up soon, we anticipate the RMB exchange rate to stabilize in the future.

There has been widespread debate this year about the possibility of a “balance sheet recession” in China. What is your view?

I don’t think China is witnessing a “balance sheet recession.”

The current consumption slowdown has something to do with income slowdown and weaker expectations. The leverage ratio of households — measured by debt to income — documented 63.3% by the end of the first quarter of 2023. That was 1.4 percentage points higher than the last quarter of 2022.

There is a substantial difference between what is going on in China and the Japanese real estate crisis from 1980s to 1990s. One important aspect to note is that the performance of China’s real estate market is triggered by policy regulation, aiming at cooling down the property market intentionally and leaving more room for transition of the country’s growth model, instead of an endogenous collapse of the market.

Another vital difference lies in the way property market adjusts. In China, housing price adjustment is moderate in general. The property market is gradually stabilizing, with some fluctuations.