European banks which rely on deposits supplied by third-party platforms should face tougher liquidity requirements to stem the risk of future hot money outflows, according to a senior official.

After hundreds of billions of dollars in customer funds flowed out of US regional lenders this year, the small-but-growing phenomenon of brokered deposits is one aspect of bank liquidity that’s gaining increasing scrutiny, on the grounds that customers can easily yank their money to find the highest bidder using online platforms.

“When I see banks relying on brokered deposits, I really worry,” Tom Dechaene, a member of the European Central Bank’s Supervisory Board, said in an interview from Brussels. “I cannot think of any more volatile deposits than that.”

Read More: ’Hot Money’ Scorches Regional Bank Profits After Deposit Flight

The rescue of Credit Suisse in March and collapse of US lenders including Silicon Valley Bank has thrown into question how well prepared banks are to withstand funding outflows. The assumed “stickiness” of deposits — the degree to which customers will stay with their bank through times of trouble or despite higher rates elsewhere — is being re-thought in an era when cash can be shifted via an app in seconds rather than by lining up at a physical branch.

Dechaene cited the example of Berlin-based fintech Raisin, which has almost doubled the money it administers in a year, as evidence that some lenders are increasingly sourcing deposits in this way.

“We should differentiate the liquidity coverage ratio requirements for those banks more than we do today,” he said. Dechaene is also member of the board of directors at the National Bank of Belgium.

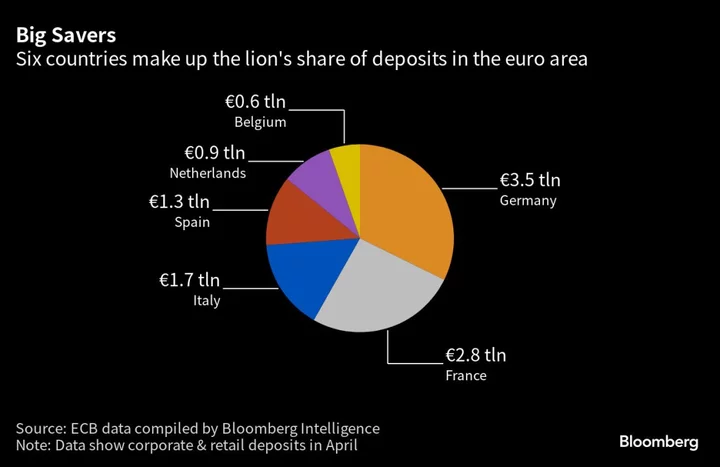

While a number of smaller US lenders source between 10% and 30% of their funding through brokered deposits, according to regulatory filings, there’s little comparable data publicly available in Europe. Raisin’s €40 billion ($43.5 billion) in assets under administration compares with a retail and corporate deposit base of more than €12 trillion in the euro-area.

“For the whole banking sector that amount is still not substantial,” Dechaene said of the funds Raisin helps place. “But in the current interest environment, with clamoring in many markets for banks to raise deposit rates, the temptation is bigger than ever before. I would be extremely surprised if in 12 months brokered deposits had not grown a lot.”

The platform says Deutsche Bank AG and UniCredit SpA are among the more than 400 banks it works with.

Stress Scenarios

A spokesman for Raisin said the firm is “often met with the misconception that platform retail deposits would come with risks for the market. Actually, the contrary is the case.”

Working with Raisin allows banks to strengthen and diversify the sources of their liquidity, the spokesman said in a response to questions from Bloomberg. The firm focuses on deposits under the statutory deposit guarantee limits, meaning “there is no concentration and the transmitted deposits are highly sticky in stress scenarios.”

Dechaene argues that brokered deposits are by nature flighty, and allow depositors to avoid taking a view on how safe the institution they’re parking their funds with is.

Clients placing money via brokered deposits is “really saying ‘I couldn’t care less how sound the bank is, I’ll just put in €99,999 and the national deposit guarantee system will take care of the rest’,” said Dechaene. “It might end up being a race between countries which have the strongest deposit guarantee systems.”

European countries oblige their banking industries to guarantee that deposits of as much as €100,000 per client per lender will be repaid if a firm goes out of business. Some national banking associations offer additional coverage.

Dechaene said some of his colleagues on the ECB’s supervisory board are similarly attentive to brokered deposits “but most of us are still more focused on capital than liquidity.” The Belgian said he supports imposing higher requirements for the liquidity coverage ratios of certain banks in the ECB’s review this year of the risks banks face.

European banks have to hold more high-quality liquid assets than they would expect to see flow out over 30 days of stress. The ECB has the power to increase that requirement, known as the LCR. The weighted average ratio for European banks stood at 165% in the fourth quarter, according to the European Banking Authority.

“I see more and more banks that in my view blatantly say 110% LCR is fine for us,” said Dechaene. “In a way that’s saying we will sail very close to the wind and if there’s a problem, we will basically knock at the door of the central bank. I have a problem with that.”

The ECB’s oversight arm is preparing for a change in leadership when Andrea Enria steps down at the close of his five-year non-renewable term in December. Dechaene said that while he did not apply for the job, he wants the next chair of the Supervisory Board to differentiate more between the banks risks face and treat liquidity risks as a higher priority.