Global financial markets already rattled by elevated interest rates now face a fresh dose of geopolitical uncertainty following Hamas’s surprise attack on Israel.

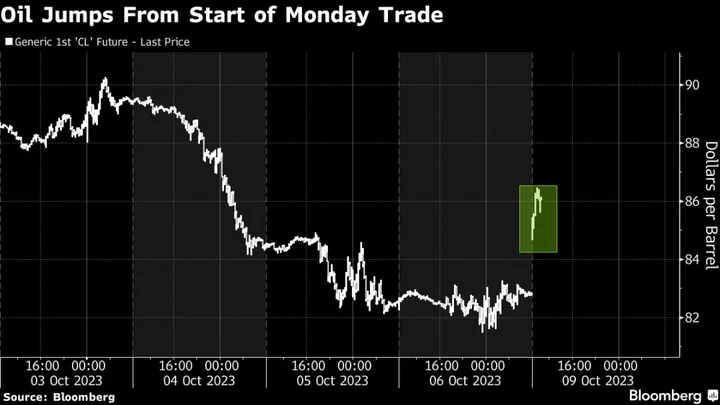

Saturday’s strike and Israel’s subsequent declaration of war threaten to unnerve markets, while a jump in crude oil from the start of Asian trade adds to concern about elevated inflation.

The yen and dollar — both haven currencies — strengthened as the trading week began following the deadly attacks. Norway’s krone advanced against all its Group-of-10 peer as it benefited from rising oil prices.

US stock futures dropped 0.7% in early Monday trade, while Asian stocks were mixed. Major equity gauges in the Middle East slid Sunday, led by a 6.4% drop on Israel’s benchmark TA-35 stock index, its biggest loss in more than three years.

Bond traders will need to quickly determine if the clash is a reason to rush for the safety of the dollar, shunning higher yielding-debt, or to fear yet another bout of inflation. Treasury futures climbed from the start of Monday trade, while cash Treasuries are shut for a US holiday.

“Geopolitical crises in the Middle East have usually caused oil prices to rise and stock prices to fall,” said Ed Yardeni, president of Yardeni Research Inc. “Much will depend on whether the crisis turns out to be another short-term flare-up or something much bigger like a war between Israel and Iran.”

Here is a roundup of responses from analysts to the weekend’s news:

Gonzalo Lardies, senior equities fund manager at Andbank

“This will add more uncertainty to markets, with inflation and growth taking a step back and geopolitical risk taking center stage. We could expect a spike in volatility, with short-term fixed income becoming again a safe haven, while in cyclical sectors will be in the spotlight.”

Guillermo Santos, head of strategy at Spanish private banking firm iCapital

“The consequences of all this should not be especially negative for the financial markets as long as the stability of the region and Iran’s violent expansionism in the field of security do not further complicate the conflict and it is limited to Palestinians and Israelis.

“It is evident that any extension of this to oil-producing countries, Saudi Arabia in the lead, could make the price of crude oil more expensive with negative inflationary effects for the West and would mean higher rates for longer and falling stock markets if the above caused a recession.”

Alfonso Benito, chief investment officer at Dunas Capital:

“I don’t expect the situation to have a meaningful impact on markets. This is a long standing terrible situation but other than some short term volatility it shouldn’t have a big impact.”

Richard Flax, chief investment officer at Moneyfarm:

“The conflict has the potential to hurt broad market sentiment, but it’s not for certain. We think a lot will depend on whether the conflict is contained or widens in scope - for instance on Israel’s northern border - and that could prompt increased concerns about commodities - oil in particular. The oil price has been quite volatile in recent weeks, and another spike could feed into consumer prices in the coming months.”

Damien McColough, head of fixed-income research at Westpac Banking Corp. in Sydney:

“Flight-to-quality probably also marries with a bit of ‘selloff exhaustion,’” he said of Monday gains for bonds in the face of surging crude oil prices

Anthi Tsouvali, multi-asset strategist at State Street Global Markets:

“The timing of the conflict could not have been worse given the talks between Saudi Arabia and Israel. A conflict in the Middle East has obvious implication in oil prices. Markets will worry about higher energy prices and since we are already in a risk-off environment, that could push equity markets lower.”

“However, given where we are in the business cycle and already slowing global demand, the impact of the conflict would not be as severe as in the previous energy crisis in 1973 as we could potentially see more Saudi Arabian capacity coming into the market if needed to meet demand. Equity markets should see through this in terms of repricing risky assets but sentiment has the potential to stay subdued for longer as the market narrative shifts from soft landing to higher-for-longer and in the long run that would be bad for equity markets.”

George Lagarias, chief economist at Mazars:

“The number one risk for the global economy is the possibility of a third inflation wave, just as the current one is petering out. The flaring of tensions in the Middle East could drive energy prices higher, and undermine the efforts of central banks to bring inflation under control. The geopolitical status quo has become increasingly unbalanced in the past few years, so outcomes from this new crisis could be more open-ended than markets may wish to believe.”

Thomas Hayes, chairman of Great Hill Capital LLC:

“In the short term, we may see a bit of volatility, but when you step back and look company by company as to whether a regional conflict will effect their earnings power — in most cases the answer is no. It’s an unfortunate circumstance but will have little to no impact on aggregate earnings power.”

John Leiper, chief investment officer at Titan Asset Management:

“While the geopolitical set-up is very different to the early ‘70s in the region, there is a real risk that we see a strong reaction from Israel that will upset the Saudi-led negotiations and could see the US bolstering sanctions against Iran, which would see the oil price rise from here. Recent supply restrictions, low US strategic reserves and stronger-than-expected non-farm payroll numbers Friday suggest oil prices could breach 100 dollars a barrel and the recent escalation in tensions add further impetus to that narrative, which may result in a further near-term spike beyond that level.”

Mansoor Mohi-uddin, chief economist at Bank of Singapore Ltd.:

“Financial markets will worry about the risk of higher oil prices pushing up global government bond yields. If the conflict widens across the region then oil supplies may be threatened. Any detente between Israel and Saudi Arabia and the potential for increased Saudi oil production will not be possible for either country to undertake if Israel and Palestinians are fighting.

“If Iran is perceived to be have spurred the hostilities in Gaza and southern Israel then the US is likely to tighten the enforcement of existing sanctions on Iran’s oil exports. All these factors would likely push oil prices up in the near term and therefore increase inflationary fears globally.”

Andrea Tueni, head of sales trading at Saxo banque France:

“I don’t expect a huge impact on European or US markets. The geopolitical risks are of course important depending on how the scale of the conflict evolves. Local stock markets are of course reacting to it but I don’t expect the same impact tomorrow.

“The only asset class one can look to for a possible reaction is oil but I don’t expect a big surge in prices given there is no impact on supply at the moment. One can’t compare the situation for oil with 1973. If the conflict was to take another dimension if for instance Israel were to directly hit Iranian infrastructure, it would be a whole different story but at the moment it is too early.”

--With assistance from Eddie van der Walt, Isabelle Lee, Katie Greifeld, Julien Ponthus and Michael G. Wilson.

Author: Macarena Muñoz, Sagarika Jaisinghani and Netty Ismail