New Zealand’s annual current account deficit unexpectedly narrowed in the first quarter as the return of tourists and international students following the pandemic boosted services exports.

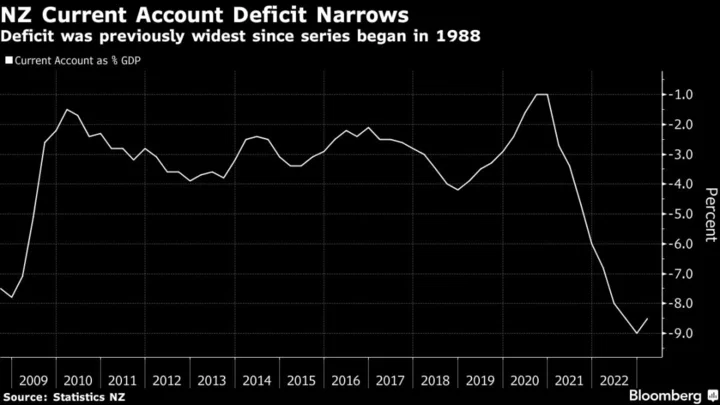

The gap came in at 8.5% of gross domestic product, down from an upwardly revised record 9% three months earlier, Statistics New Zealand data showed Wednesday in Wellington. Economists expected the deficit to widen to 9% from the initially reported reading of 8.9%, according to a Bloomberg survey.

New Zealand’s current account deteriorated as massive fiscal and monetary stimulus delivered during the pandemic swelled imports. S&P Global Ratings warned in March that its AA+ foreign currency credit rating for New Zealand could come under pressure if the deficit remains too large.

The gap widened from 6% at the end of 2021 and just 1% at the end of 2020. By comparison, Australia runs a surplus. The current account is the broadest measure of trade as it includes services such as tourism and investment flows.

The deficit shows that New Zealand is living beyond its means, said Miles Workman, senior economist at ANZ Bank New Zealand in Wellington.

“However, reopened borders and monetary tightening, which will weigh on domestic demand and therefore imports, mean the deficit should narrow further from here,” he said. “That’s something sovereign credit rating agencies are likely to be keeping in mind as they assess New Zealand’s external sector sustainability.”

The deficit was NZ$33 billion ($20.3 billion) in the year through March, down from NZ$34.4 billion in the 12 months through December, the statistics agency said.

The annual goods deficit widened to NZ$13.6 billion from NZ$12.5 billion in December. The services deficit in the year through March was NZ$7.4 billion, down from NZ$9.6 billion in December.

The current account deficit was NZ$5.2 billion in the first quarter, almost half the upwardly revised fourth-quarter figure of NZ$10.1 billion.