Japan’s interest rates have been grounded for 30 years. Now one bank is seeking people with 1980s-era experience akin to aviator Pete “Maverick” Mitchell to navigate their take-off.

While it may be a stretch to liken regional banking to the dogfighting of Tom Cruise’s Top Gun character, that’s exactly how Tatsuya Kataoka describes his bank’s challenges in anticipation of borrowing costs finally rising in coming years.

“Rates have been falling since the 1990s,” said Kataoka, 56, who joined Concordia Financial Group Ltd. in 1990 and became its president last year. “There are very few who experienced rising rates, not just at our bank, but probably at others.”

Like many in the market, Kataoka doesn’t expect the Bank of Japan’s negative-rate policy to end in the immediate future, but he said he needs to be ahead when the eventuality comes. “Whether financial institutions can prepare before rates start rising determines the winners and losers five years down the road.”

Talent is one of the biggest management challenges, according to Kataoka. Concordia, which owns Bank of Yokohama Ltd. and is one of Japan’s biggest regional lenders, has been hiring people and nurturing young employees through trainee programs to beef up its markets operations and help to manage its 3 trillion yen ($21 billion) securities portfolio.

“Those who know the markets of the 1980s and early 90s, who were in the dealing room when rates were rising, are becoming fewer. We need to have such veterans as advisers,” he said. “But to be honest, we haven’t been able to find any.”

Asked whether he meant someone like the main character in Top Gun: Maverick, Kataoka said “Yes, you can say that. Someone who can fly the fighter manually,” referring to the scene in which Maverick commandeered an old F-14 Tomcat fighter.

Read how old-school JGB voice brokers are coming back

In the 1980s, the yield on the 10-year JGBs ranged from about 2.5% to 7%, making it essential to have nimble and highly skilled traders. More recently, the BOJ’s monetary easing has kept the benchmark below 1% for over a decade, and most traders have never experienced a major surge in rates that would put them at risk of large writedowns.

Kataoka’s bank has already learned a hard lesson on what can happen when you go into a rate-rising phase unprepared. Concordia is one of many Japanese lenders that were caught off guard by the US Federal Reserve’s rapid rate hikes last year, which forced them to dump foreign bonds at a loss. Some US regional lenders fared even worse, with Silicon Valley Bank and First Republic Bank among those to fail.

Kataoka said the bank has tightened its risk management. His bank got rid of loss-making foreign bonds and is set to rebuild its securities holdings. “Market volatility is high, so we are now discussing what our portfolio should be right now,” he said.

Read about what helped Japan banks withstand SVB scare

The bank is “very cautiously” building up collateralized loan obligations and other foreign debt products, he said. Its CLO holdings stood at about 170 billion yen at the end of June, up from 150 billion yen three months earlier.

Kataoka said the bank is paying close attention to credit risks of these products. “We are investing within the scope of manageable risks,” he said.

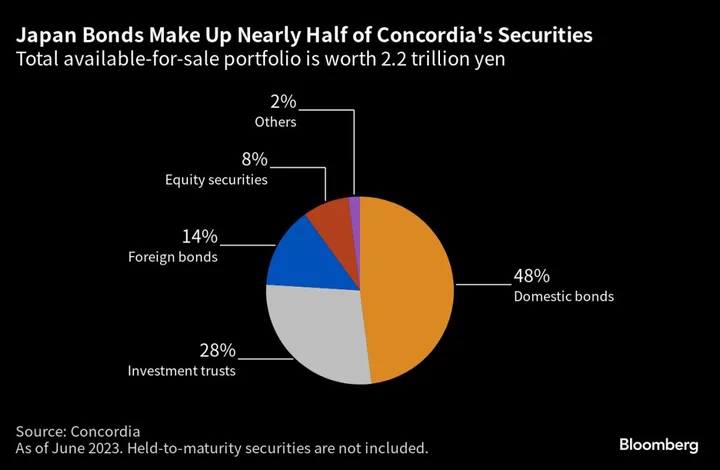

Concordia is also gradually increasing Japanese government bonds that are held to maturity and relatively short-term ones in the available-for-sale portfolio, as yields tick higher.

“We need to be careful about the speed and timing of the build-up” in holdings, Kataoka said, referring to the BOJ’s surprise tweak to its yield curve control program in July.

The impact of the BOJ’s interest-rate policy isn’t limited to the bank’s securities portfolio. Its traditional loan and deposit businesses are also likely to see major shifts.

The introduction of the negative-rate policy seven years ago has made deposits less attractive for Japanese banks. Besides squeezing the spread between what they receive on loans and pay on deposits, it meant they have to pay to hold excess reserves at the central bank. The opposite will happen if rates start climbing.

“If interest-rate conditions begin to change, the scale of deposits and assets will become very important,” Kataoka said.

--With assistance from Brett Miller and Issei Hazama.

(Updates with CLO holdings in the 11th paragraph)