Bond traders got a glimpse this week of what the eventual end of the Federal Reserve’s hiking cycle may look like.

Amid volatile trading conditions, Treasuries had their best week since mid-July after several central bank officials observed that a selloff that had driven yields to multiyear highs was advancing the Fed’s aims in a way that might prevent additional tightening. Yields plummeted as those comments, combined with haven demand stoked by Middle East conflict, painted a more supportive backdrop for US bonds.

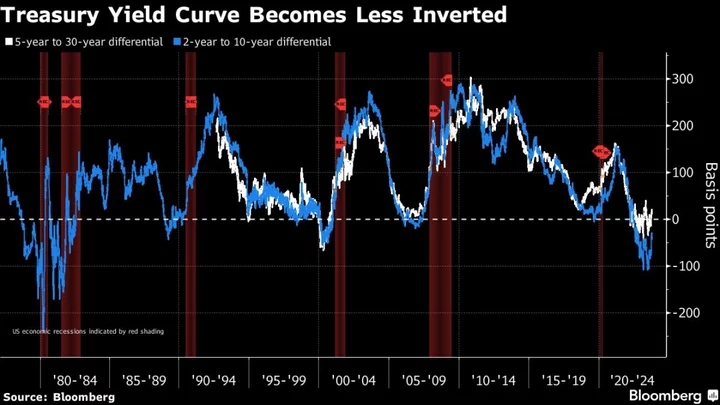

It was a sharp about-face. The rise in yields in recent weeks had seemed unstoppable, predicated on the Fed’s policy rate remaining elevated indefinitely. But despite the week’s rally, many investors are sticking with their expectations for higher-for-longer rates and see recent gains as fragile. Emboldened by poor Treasury auction demand, they’re looking for long-term yields to rise further, and eventually moving back to above short-term ones, where historically they’ve belonged.

“It’s being in restrictive territory that matters,” Greg Peters, co-chief investment officer of PGIM Fixed Income, told Bloomberg Television Thursday. “The curve will continue to normalize. You’ll definitely see back-end rates moving higher, maybe there’s a little scope over the next 12 months for the front-end to move lower, but not a lot. I just think we have to move into this more normal environment.”

The fragility of the Treasury market’s advance was in full view Thursday when gains were swept away by data showing that US inflation remains elevated, and from anemic demand for an auction of 30-year bonds, despite offering the highest yield since 2007. The odds of one more quarter-point hike later this year or by January rebounded, while the scope of rate cuts for 2024 eroded.

Also, while a 12th Fed interest-rate increase is still considered less likely than a coin flip, several policy makers this week said they’re open to raising rates further if necessary.

What Bloomberg’s Strategists Say...

“The lion’s share of the recent spike in long-term yields is explained by changes in market participants’ perception of the Fed’s monetary policy stance. Risk sentiment and fears of inflationary supply disruptions also play a role.”

“October’s mid-month auctions will provide another glimpse into investor’s appetite for additional duration risk as Treasury supply narratives continue to weigh on markets.”

— Ana Galvao, senior economist, Bloomberg Intelligence

Click here for the full report

Haven demand bolstered the market Friday, with escalating Middle-East warfare stoking global recession fears. US economic fundamentals remain challenging for now, though, and Treasury supply is an ongoing source of angst.

Consumer price growth failed to moderate as much as economists estimated in September, Thursday’s data showed, while the separate inflation rate the Fed is trying to bring back to 2% quickened to 3.5% back in August.

Even at a recent peak of 4.88%, the 10-year yield “was still very much priced for a 2% inflation world,” Oksana Aronov, head of market strategy for alternative fixed income at J.P. Morgan Asset Management, said on Bloomberg Television Thursday. “So I wouldn’t be surprised if the 10-year does cross 5%.”

As for supply, Treasury debt auctions were increased in size for the August-to-October quarter for the first time in more than two years, and another round of increases is anticipated for November-to-January, to be announced on Nov. 1.

Expanded borrowing at a time of low unemployment “is a very worrying position and is really unusual at this stage of the cycle,” said Gene Tannuzzo, global head of fixed income at ColumbiaThreadneedle. He also is concerned about the potential for oil prices to keep upward pressure on inflation and long-term yields.

Read More: Pimco Sees Bonds Benefiting as Markets Overlook Recession Risk

Still, this week’s brief reprieve illuminated the inherent risk of hiding out in cash while waiting for long-term yields to peak — the profitable course for most of the past three years.

“I do sense that clients still favor shorter duration since fixed-income has been so painful for so long now,” said Baylor Lancaster-Samuel, chief investment officer at Amerant Investments Inc. “There will be a moment when you will wish you had duration, and while we don’t know exactly when that will be, I have not been as excited about fixed income in my two decades on the street.”

What to Watch

- Economic data calendar

- Oct. 16: Empire manufacturing; monthly budget statement

- Oct. 17: Retail sales; industrial production; Treasury international capital flows

- Oct. 18: MBA mortgage applications; housing starts; Fed Beige Book

- Oct. 19: Initial jobless claims, Philadelphia Fed business outlook; existing home sales; Leading Index

- Fed calendar

- Oct. 16: Philadelphia Fed President Patrick Harker

- Oct. 17: New York Fed President John Williams; Fed Governor Michelle Bowman; Richmond Fed President Tom Barkin; Minneapolis Fed President Neel Kashkari

- Oct. 18: Fed Governors Christopher Waller, Bowman and Lisa Cook; Williams, Barkin and Harker

- Oct 19: Fed Vice Chair Philip Jefferson, Fed Chair Jerome Powell; Chicago Fed President Austan Goolsbee; Atlanta Fed President Raphael Bostic; Harker; Dallas Fed President Lorie Logan

- Oct. 20: Harker; Cleveland Fed President Loretta Mester

- Auction calendar:

- Oct. 16: 13- and 26-week bills

- Oct. 17: 42-day cash management bills

- Oct. 18: 17-week bills; 20-year bonds

- Oct. 19: 4- and 8-week bills; 5-year TIPS

--With assistance from Edward Bolingbroke.

Author: Michael Mackenzie, Ye Xie and Liz Capo McCormick