Behind the facade of Europe’s forecast-beating company earnings, cracks are appearing as exporters start to feel the pinch from regional exchange rate strength against the dollar.

The euro, Swiss franc and sterling are predicted to rise further versus the US currency, potentially spelling trouble for the Stoxx 600 equity index which, according to data compiled by Bloomberg, relies on North America for nearly a third of its sales.

So far, the effect is not fully apparent — despite the euro’s 13% gain versus the greenback since its September low, the majority of Stoxx firms have surpassed first-quarter earnings estimates. Dig deeper though, and it becomes clear that swathes of companies, especially exporting conglomerates such as Bayer AG and Roche AG, are feeling the pain.

This could ripple out more broadly in coming months, if support fades from China’s post-Covid reopening, Europe’s hitherto resilient growth slows and the US tips into recession.

“Economic strength has disguised the impact of currency appreciation,” Sharon Bell, senior European equity strategist at Goldman Sachs Group Inc. “But it will be coming through, we expect to see more impact in the second and third quarter.”

As a rule of thumb, Bell says, a 10% rise in the euro shaves 2% to 3% off earnings-per-share growth for European companies. This impact will be increasingly hard to avoid, she reckons, especially as the bottoming of exchange rates last September sets a steep bar for year-over-year comparisons.

Bloomberg Intelligence sees the euro touching $1.20 against the dollar by year-end, while sterling and the Swiss franc are also expected to strengthen versus the greenback. Analysis of CEO calls by Barclays Plc, showed less than 40% of companies now have a positive view on exchange rates, down from over 60% in the third quarter of 2022.

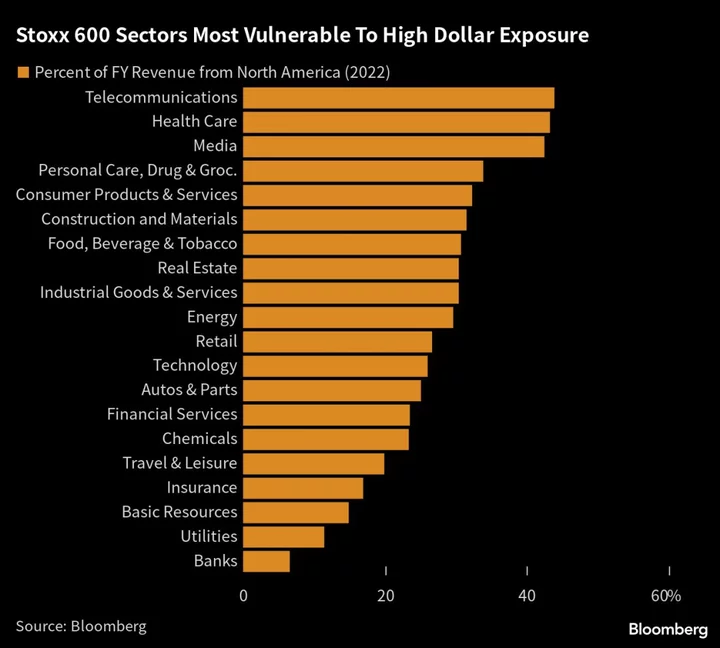

Vulnerable sectors

Europe’s telecommunications, health care, media, and consumer staples companies receive the greatest proportion of their revenue from North America, according to analysis by Bloomberg.

For such businesses, strong currencies are a double-edged sword. They help dampen imported inflation, crucial at a time when companies are reeling from high input costs. But they can make goods more expensive for buyers in other countries, and mean overseas earnings are worth less when translated into the local currency.

Germany’s Bayer, for instance, warned of a €1.7 billion exchange-rate hit in 2023, with full-year sales potentially coming in at the bottom of a previously forecast range. Chief executive officer Werner Baumann reassured analysts that hedging efforts have been ramped up to protect the bottom line.

At Switzerland’s Roche, which relies on the US market for half its revenue, chief financial officer Alan Hippe said first-quarter sales had fallen 3% in constant exchange-rate terms. But taking into account currency moves, the decline amounted to 7%.

Another example is Dutch retailer Koninklijke Ahold Delhaize N.V. With 60% of revenue coming from North America, chief financial officer Natalie Knight does not expect full-year EPS to grow from 2022, citing moves in the US dollar as a reason.

Read more: Wild Currency Swings Shaved $29 Billion Off of Corporate Profits

Regional upside

As European boardrooms brood about the impact, dollar-based American investors are reveling in the extra windfall they can earn from the exchange-rate translation.

Vanguard’s FTSE Europe ETF, the largest unhedged US-based fund geared to European shares, has received over $19 billion this year as investors buy into the region’s stocks.

“Currency strength has been a big building block for our neutral to bullish view on European equities, relative to the US,” said Alessio de Longis, a New-York based fund manager at Invesco.

De Longis sees the euro strengthening to $1.20-$1.30 on a multi-year period, but does not expect a material impact on short-term corporate earnings. “Currency valuations affect equity markets with a different time lag,” he said, noting the euro has been undervalued for years.

In Europe, some money managers are adjusting their positions to account for the currency shifts. Alexandra Jackson, manager of the Rathbone UK Opportunities Fund, prefers the domestically oriented FTSE 250 index to the internationally exposed FTSE 100.

Swiss companies are probably better positioned than others, given their track record of operating under a strong franc, according to Eleanor Taylor-Jolidon, a portfolio manager at Union Bancaire Privee in Geneva. She is more dubious of broader European stocks’ ability to withstand currency pressures, noting that recent euro moves are “more a product of dollar weakness than fundamental strength.”

--With assistance from Jan-Patrick Barnert, Blaise Robinson and Michael Msika.