Employers are losing trust in the companies they hire to run their health plans.

Kraft Heinz Co. accused CVS Health Corp.’s Aetna of wasting its money by paying fraudulent medical claims. Two union health insurance plans in Connecticut alleged that insurer Elevance Health Inc. routinely overpaid medical bills. And the trustees of a bankrupt trucking company accused insurer UnitedHealth Group Inc. of mismanaging millions of dollars.

After years of ever-inflating medical costs, American companies and union benefit plans have alleged in a series of lawsuits that the country’s biggest health insurers are squandering their money. What’s more, they argue that insurance companies refuse to hand over critical information about their medical claims when asked.

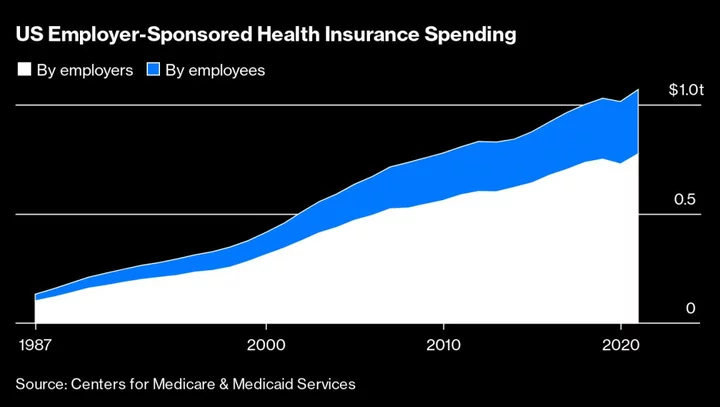

The cases reveal an emerging rift between employers that spend $1 trillion a year on health benefits and the insurance firms they hire to operate those plans: Some companies increasingly want to know where their money is going and what prices they pay for care, but insurers say they must keep those details private to stay competitive.

“It kind of makes you wonder, is there something that they're hiding that they won't release this information?” said Michael Thompson, a trustee who represents union contractors that pay into the Connecticut unions’ health plans suing Elevance.

Aetna, Elevance and UnitedHealthcare declined interview requests and wouldn’t comment on the cases. Elevance and UnitedHealthcare disputed the allegations in court filings, while Aetna hasn’t filed a reply yet.

Health insurance is usually the most expensive benefit employers offer, and the cost typically rises faster than wages or inflation. The annual price of insuring a family, counting employers’ and workers’ contributions, now exceeds $22,000 — up 20% in the last five years alone. To manage, employers have shifted more costs onto workers by requiring bigger monthly contributions and using high-deductible plans that leave people paying more for medical bills.

Until recently, most employers haven’t been probing the insurance companies’ role in rising costs, at least not in any public way. Insurers have long argued that their job is to get the lowest prices possible for employers by negotiating with doctors and hospitals. New transparency rules require hospitals and health insurers to publicly disclose the prices they’ve negotiated for many services, giving employers the data that’s causing them to ask some of these questions now. In a handful of instances that have landed in court, insurers have argued in their defense that the deals they strike with medical providers are confidential, and that employers have agreed to limits on how they can access claims data.

But when employers dug in, some said they found discrepancies they couldn’t ignore. The Connecticut union groups’ insurer, Elevance, was supposed to get the health plan a 50% discount from hospital charges, but instead they found some bills paid at double what the hospital charged, according to their joint lawsuit filed in December in federal court in Connecticut. The plaintiffs — the entities who pay for and oversee the unions’ health benefits — are seeking class action status, to represent other self-funded health plans that hired Elevance.

In one instance, the International Union of Bricklayers and Allied Craftworkers Local 1 paid $43,490 for a procedure billed as a skin graft at Hartford HealthCare, more than twice Elevance’s negotiated rate, according to the complaint. The unions pressed Elevance, formerly called Anthem, for detailed claims data to figure out what was going on. But the insurer resisted handing it over, according to the Connecticut unions’ lawsuit.

Read More: The Hospital Bill Was $674,856. Why Did the State Pay More Than $2 Million?

The insurer argued it was abiding by its contract and asked the court to dismiss the case. Elevance said in court filings that the groups had agreed to restrictions on accessing this data in their contracts and “now contend that the contractual requirements for data reporting and audits that they negotiated are too restrictive.”

The insurer argued the unions relied “on a misconstrued observation of differences between some unidentified subset of their claims data and negotiated rates posted on the internet by certain hospitals.” Elevance said that the hospitals’ publicly listed prices aren’t always supposed to match what the insurer pays.

The trustees who oversaw the Connecticut union plans have been scrambling to cover rising expenses. One redirected money from retirement funds. Another added a $4,000 deductible for members just so they could afford to keep offering a health plan. Some workers split pills to stretch their prescriptions longer, or even skipped them entirely, according to the unions.

Who Pays What

Most large US employers are self-insured, meaning they pay for workers’ medical claims themselves. They rely on outside companies — arms of big health insurers — to negotiate rates with doctors and hospitals and make payments for them. They also pay an administrative fee to the insurers, usually a set amount per member, for day-to-day plan operations like processing claims and running call centers.

Employers and unions that offer health benefits face rising pressure to ensure that they’re not wasting workers’ money on unreasonable fees to middlemen or by overpaying for care. Congress amended the law that governs those plans — the Employee Retirement Income Securities Act — to strengthen oversight in 2020. The changes aimed to ban “gag clauses” that keep plans from knowing what they pay for specific medical claims.

Because of the new transparency laws, employers should in theory be able to compare the rates they pay for medical care to publicly reported prices and determine if they’re paying too much. But when companies have invoked the new provisions against gag clauses to compel insurers to hand over the data, some say they’ve run into resistance. The kinds of conflicts that the lawsuits describe are playing out broadly across the industry, even when they’re not winding up in court, according to employer groups.

“It’s been a nightmare of delays,” said Karen van Caulil, chief executive officer of the Florida Alliance for Healthcare Value, which represents employers in the state. Florida employers pay triple the Medicare rate for hospital care, one of the highest rates in the US, according to a Rand Corp. analysis, and van Caulil said more employers in the state are pressing for claims data to understand why. But they’re often met with months of resistance from their health plans, she said. “They are handcuffed in being able to get that information.”

Congress is considering creating tougher policies: One bill would impose penalties of $10,000 a day on health insurers that block their employer or union clients from getting information on payments, including claims data stripped of personal identifying information.

Wasted Spending

Companies and unions have good reason to ask where their money is going. About a quarter of health-care spending is wasted, according to a 2019 review of research published in JAMA — between $760 billion to $935 billion at the time. Errors are routine, according to Medicare data that shows tens of billions in improper payments every year. It’s unclear why this is happening.

Almost half the time, the median rates negotiated by insurance companies were higher than the cash prices hospitals charged, according to a recent analysis in the journal Health Affairs of prices posted by more than 2,000 hospitals. A representative of the insurer trade group America’s Health Insurance Plans called those cases “the exception” and said insurers negotiate lower costs, but declined to provide evidence. The group declined to comment on disputes between employers and insurers over reimbursement rates and access to claims data.

Kraft Heinz, which employs 37,000 people, alleged Aetna “paid millions of dollars of claims that never should have been paid” and has prevented the company from being able to figure out why, according to a lawsuit filed in June in federal court in the Eastern District of Texas. Kraft requested its claims data in November 2021. What Aetna provided, more than a year later, left out hundreds of data fields, including information that would link a medical claim to a specific payment in order for the company to see if it was billed correctly, according to the lawsuit. Aetna declined to comment. The insurer hasn’t filed a response in court yet. A lawyer for Kraft Heinz declined to comment.

In another lawsuit filed in 2021 in the Eastern District of Virginia, trustees for a bankrupt trucking company accused UnitedHealthcare and Harvard Pilgrim Health Care of making about $27 million in overpayments from the company’s funds and said the insurers thwarted attempts to audit the payments. The insurers disputed the allegations and the case was settled in June, according to a court filing.

In February, Owens & Minor, a medical-equipment supplier, sued a unit of Elevance in federal court in the Eastern District of Virginia alleging the insurer blocked the company’s attempt to get its health plan data with “a year-long trail of emails and other correspondence, littered with defendant’s excuses, arbitrary conditions, and illusory promises.” An Elevance representative said the insurer wouldn’t release billing information that would allow Owens & Minor to compare how much providers charged versus how much was paid for the services, according to the complaint. Elevance said in a legal filing that its contracts with providers are confidential. The case is in talks to be resolved, according to a joint notice filed July 12 saying both parties expect to seek dismissal.

Fiduciary Debate

How these lawsuits play out may hinge on how courts view the relationship between insurers and their clients. The employers and unions argue that insurers are what’s known as “fiduciaries,” responsible for ensuring employee health funds are spent prudently — the same way managers of retirement plans must act in the best interest of the funds’ beneficiaries.

Read More: Health-Care Oversight Rule Changes Create Legal Risk for US Employers

But insurers facing this litigation say they aren’t fiduciaries. They say they’re following the terms of their contracts with employers and honoring payment agreements they’ve made with providers. Those contracts, insurers say, don’t require them to turn over all the data that employers seek.

This argument has prevailed before. In a 2021 lawsuit against Blue Cross Blue Shield of Massachusetts, a construction worker union fund said it uncovered thousands of claims paid incorrectly, including some above providers’ billed charges. One claim was paid at $120,614 when a hospital billed only $38,786, according to the lawsuit.

The Department of Labor got involved in that dispute, essentially siding with the union fund and arguing to the court that Blue Cross should be considered a fiduciary of the health plan. That would raise the standard it would have to adhere to when making payments with the plan’s money. An appellate court disagreed, upholding a ruling in favor of Blue Cross Blue Shield on the grounds that the insurer didn’t bear that responsibility.

That ruling shows the bind employers are now in: It leaves the employer as the fiduciaries of health plans, putting them on the hook for making sure the money is spent responsibly. But they can’t do that if insurers refuse to share the data.

Unite Here Health, a union plan that covers 200,000 service workers and their families, tried to compel its insurer Blue Cross Blue Shield of Illinois to share its claims data with Rand Corp. for a prominent study of hospital prices, but the insurer refused, according to Ivana Krajcinovic, a vice president of the union health plan. A spokesman for the insurer, Dave Van de Walle, said in an email that participation in the Rand survey “is voluntary, and BCBSIL has opted out.”

Insurers should want people to have more information on medical claims because “it should advance their work in getting the best network discounts that are possible,” said Krajcinovic. “When they’re not interested in participating in this, it makes us feel like they’re not trying very hard to keep costs down.”

--With assistance from Marie Patino.