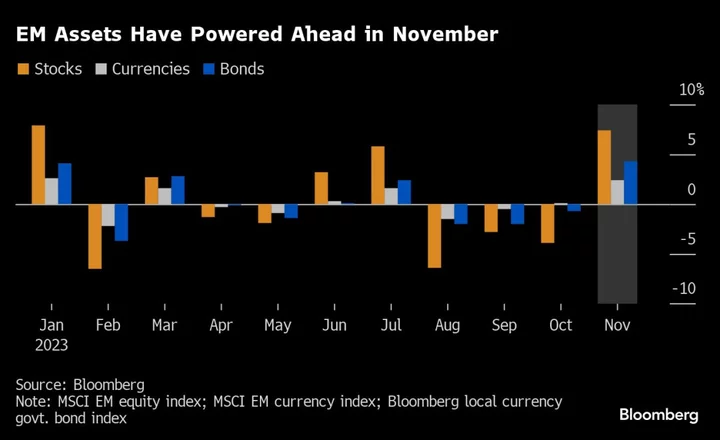

Emerging-market stocks and currencies are heading for their best month since January, but there are major pitfalls ahead that could derail the rally.

The headwinds in coming months include the risk of renewed Federal Reserve hawkishness and elections in key markets such as Taiwan and India. There’s the threat of drastic economic change under Argentina’s new president and a referendum in Chile that could spark riots. Finally, November’s big gains alone create the chance of a pullback.

“The amplitude of the November move across all risk classes has been extremely strong, so I would expect some volatility,” said Rajeev De Mello, a global macro portfolio manager at Gama Asset Management SA in Geneva. Still, he said, positive real rates and less-crowded positioning will support the upward trend in emerging-market assets.

An MSCI index of emerging-market equities has jumped 7.1% in November, and a similar gauge of currencies has risen 2.3%, both the biggest advance since January. Positive catalysts included optimism the Fed is nearing the end of its tightening cycle, and a meeting in California between US President Joe Biden and his Chinese counterpart Xi Jinping that was taken to herald an easing of geopolitical tensions.

With much of the good news now factored in, emerging markets may be vulnerable to these bearish risks:

1. Hawkish Fed

Most market watchers agree the key threat is a change in mood at the Fed, with a focus on the Dec. 12-13 meeting when policymakers are due to release their revised dot-plot projections.

Traders have trimmed bets on US rate hikes following softer-than-expected data, but it wouldn’t take much for that to reverse. Markets are anticipating more than a full percentage point of easing by the end of 2024, which may end up being optimistic if US inflation remains high.

“The main risk to emerging markets is, paradoxically, a continued strengthening in US economic growth, which could cause the Fed to resume hiking policy rates if combined with persistently high inflation,” Gama Asset’s De Mello said.

Elevated US interest rates would also strengthen the dollar and could siphon funds out of some of the bigger developing nations that saw inflows this month.

Emerging Asia’s higher-yielding bonds — Indonesia and India — have lured in a combined $2.3 billion of funds in November, the most since June.

2. Taiwan Vote

Among a number of elections due in coming months, the one in Taiwan stands out for its potential market impact.

Polls show the the incumbent Democratic People’s Party is expected to win the presidential vote on Jan. 13, an outcome seen as a negative for the island’s assets given the party favors less rapprochement with China.

The opposition campaign has been in turmoil in recent days with the implosion of a potential alliance that aimed to unseat the ruling party and install a China-friendly government.

“The two months before the Taiwan election, and the four months after that until the inauguration of the next government on May 20, will be fraught with uncertainty,” said Matt Gertken, chief geopolitical strategist at BCA Research in Montreal.

3. Other Elections

Elections are also due in Indonesia, Egypt and India, with the potential for populist spending pledges to weigh on government finances.

There are three contenders for Indonesia’s presidential vote due Feb. 14, which will see a new premier take over from Joko Widodo.

There’s uncertainty over whether the next administration will continue with Jokowi’s efforts to open up the economy to foreign investors, the commitment to central bank independence and Indonesia’s relationship with China, said Jon Harrison, managing director for emerging-market macro strategy at GlobalData TS Lombard in London.

“We are inclined to reduce exposure ahead of the election,” he said.

Egypt will hold a presidential election on Dec. 10-12, while India just began a series of provincial elections in five states in November and December, before a general election between April and May.

India’s state governments announced additional spending ahead of the votes, and there’s the risk political parties will do the same before the general election, Aditya Sharma, a strategist at Natwest Markets, wrote in a research note this month.

4. Argentina, Chile

Political developments in South America may also create a broader threat to emerging assets.

Libertarian outsider Javier Milei won a landslide victory in Argentina’s presidential runoff on Nov. 19 on a platform that included replacing the peso with the US dollar and shutting down the central bank. Argentina’s GDP slumped 2.8% in the second quarter, the deepest decline since the peak of the pandemic in early 2020.

Milei’s platform on balance is the right prescription to try and change Argentina’s economy, although execution risks are the biggest challenge due to his party’s limited representation in congress, said Brendan McKenna, an emerging-markets strategist at Wells Fargo & Co. in New York.

Still, Milei appeared to retreat from his dollarization plan this week, choosing two former Wall Street veterans to head his economic team.

Chile holds another referendum on changes to its constitution on Dec. 17, after massive demonstrations in 2019 triggered a three-year effort to replace the present document that was created during the dictatorship era. A first attempt at the new constitution was overwhelmingly rejected last year.

“I think the referendum will get voted down again, probably by a pretty wide margin too,” resulting in protests and volatility in markets, McKenna said.

What to Watch

- Taiwan, Turkey, Hungary, Poland and the Czech Republic all publish third-quarter GDP data

- Central banks in Israel, Thailand and South Korea are forecast to keep rates unchanged at scheduled policy decisions. For Thai policymakers, this would be the first rate pause in more than a year

- China’s PMI data for November will provide a guide on whether the slowing economy is starting to stabilize

- Indonesia and Poland will announce inflation figures

--With assistance from Matthew Burgess and Wenjin Lv.